Long Term Care Insurance: What It Is, What It Costs, and How It Works

Posted in Long Term Care Insurance last updated on May 26, 2026

Posted in Long Term Care Insurance last updated on May 26, 2026Seven out of ten Americans who turn 65 will need some form of long-term care before they die. Most will need it for two or more years. Many will need it for five or longer.

This is the statistical reality of living a long life in America.

The problem is that long-term care is expensive. According to a recent survey by CareScout, a private room in a nursing home now costs a national median of $129,575 per year. Assisted living costs about $ 75,000+ annually. Even home care from a full-time health aide averages $10,000 a year, and these numbers keep rising.

Without a plan, all these expenses fall directly on your retirement savings, your home equity, and ultimately your family.

Long-term care (LTC) insurance exists to transfer that financial risk from your family to an insurance company. This guide will explain exactly how it works, what it covers, who needs it, and your options so that you can make a smart, informed decision.

Quick Summary

Long-term care insurance helps cover the cost of services like home care, assisted living, and nursing homes when you can no longer perform daily activities on your own. Most health insurance and Medicare do not cover long-term custodial care, making LTC insurance a key tool for protecting retirement savings and maintaining control over care decisions. Costs vary based on age, health, and coverage level, but planning early can significantly reduce premiums.

Table of Contents

- What Is Long-Term Care Insurance?

- Who Needs Long-Term Care Insurance?

- What Does LTC Insurance Cover?

- What Does Long-Term Care Actually Cost? (2025 Data)

- Will Medicare or Health Insurance Pay for Long-Term Care?

- Types of Long-Term Care Insurance

- How Does LTC Insurance Work?

- How Much Does LTC Insurance Cost?

- How to Choose the Right Long‑Term Care Insurance Policy

- Planning Ahead: When to Buy and What to Expect

- Alternatives to Long‑Term Care Insurance

- FAQs

- Taking the Next Step: Protecting Your Future

What Is Long-Term Care Insurance?

Long-term care insurance is a type of coverage that pays for the assistance you need when a chronic illness, disability, or the effects of aging make it impossible to handle basic daily tasks on your own. These tasks, often called Activities of Daily Living, or ADLs, include eating, bathing, dressing, toileting, continence, and moving from a bed to a chair. Moreover, a diagnosis of cognitive impairment, such as Alzheimer’s disease or dementia, also qualifies, even if the person can still physically perform the ADLs.

Long‑term care is not hospital care or acute medical care. It is custodial support that allows a person to live as independently as possible. In‑home care aides can assist with meal preparation and personal care, while assisted‑living facilities and nursing homes provide 24‑hour support. Medicare and most health insurance plans do not pay for extended custodial care, so families are often responsible for the full cost.

Long‑term care insurance is an insurance product designed to pay for these services when you need them. Policies pay a daily or monthly benefit up to a specified amount if you can’t perform at least two activities of daily living or suffer from a severe cognitive impairment.

The monthly benefits can be used for in‑home care, adult day services, assisted‑living, nursing home care, and even hospice care. Without coverage, many older adults must “spend down” their assets to qualify for Medicaid. All in all, long-term health care insurance helps preserve your savings and gives you more choices about where you receive care.

Want to go deeper? Our full guide explains exactly what qualifies as a benefit trigger and how the claims process works. What Is Long-Term Care Insurance? (How to Protect Your Nest Egg From Old Age)

Who Needs Long-Term Care Insurance?

Long-term care insurance is not for everyone. But for the majority of pre-retirees and retirees, the risk of needing care and the financial damage it can do is real enough to have a serious look.

You’re a strong candidate if you:

- Are between the ages of 45 and 65 and in reasonably good health

- Have accumulated retirement savings or assets you want to protect

- Own a home or other assets that could be wiped out by care costs

- Want to preserve an inheritance for your children or grandchildren

- Want to maintain choice and control over where and how you receive care

- Don’t want to burden your spouse or children with caregiving responsibilities

LTC insurance may not be necessary if you:

- Have very limited assets and would qualify for Medicaid with minimal spend-down

- Have substantial enough wealth (typically $5 million or more) to self-insure

- Have significant health conditions that make coverage unavailable or cost-prohibitive

For the majority of Americans between these extremes, such as those who have worked hard to build a nest egg but couldn’t absorb a $100,000+ annual care bill without depleting it, LTC insurance is often the most cost-effective way to protect what they’ve built.

If you’re on the fence, the best step is to get a personalized long-term insurance quote and speak with an advisor. Waiting often means higher premiums or an unexpected health event that makes you uninsurable.

What Does LTC Insurance Cover?

One of the biggest misconceptions about long-term care is that it only happens in a nursing home. In reality, care can, and often does, happen in many different settings.

Most LTC insurance policies cover services provided in:

Home Care (In-Home Care)

Home-based care allows you to stay in the comfort of your own space while receiving help from a qualified caregiver or nursing assistant. This preferred option covers everything from personal grooming to light housekeeping. It’s important to note that while most policies pay for these professional services, they generally won’t cover care from relatives unless they hold a professional license.

Nursing Homes (Skilled Nursing Facilities)

Also called nursing homes, these facilities provide the highest level of support for those who need round-the-clock medical attention. These facilities offer a safe, supportive environment with 24-hour supervision from licensed nurses and therapists, ensuring your loved one is never alone in their care. While this is often the most significant investment in terms of cost, it provides comprehensive professional nursing care in both private and semi-private settings for those who can no longer live independently.

Assisted Living / Residential Care Facilities

Residential communities that provide a comfortable middle ground for those who want to maintain their independence while having a helping hand nearby. In these communities, residents enjoy the privacy of their own rooms or apartments, paired with the peace of mind that comes from having professional support for daily activities, shared meals, and medication management.

Adult Day Care Centers

These facilities offer a welcoming environment where your loved one can enjoy social activities, nutritious meals, and professional supervision throughout the day. It’s a wonderful way to ensure they are safe and engaged, while also giving family caregivers the essential time they need to work or attend to other responsibilities, knowing their relative is in good hands.

Memory Care Units

Specialized, nurturing communities designed specifically for those living with Alzheimer’s or other forms of dementia. These spaces prioritize both safety and dignity, featuring secure environments and thoughtful daily programming tailored to each individual’s cognitive journey. It’s a supportive setting that focuses on celebrating what a loved one can still do, while providing the specialized expert care they deserve.

Hospice and Respite Care

Every family deserves an extra layer of professional kindness during challenging times. Many policies include respite care to provide family caregivers with an essential break, allowing them to rest while their loved one is looked after by experts. When the focus shifts to life’s final transitions, hospice care ensures that comfort and dignity remain the highest priority, surrounding the family with a nurturing environment of expert care.

Learn the full details of coverage: What Does Long-Term Care Insurance Cover? A Comprehensive Guide

As you explore your options, keep in mind that policies often differ in how they provide support, whether through expense reimbursement or a flexible cash benefit. Some also include extra perks, such as caregiver training or home updates. Reading through your policy details ensures you understand these features, giving you the clarity and peace of mind you deserve.

What Does Long-Term Care Actually Cost? (2025 Data)

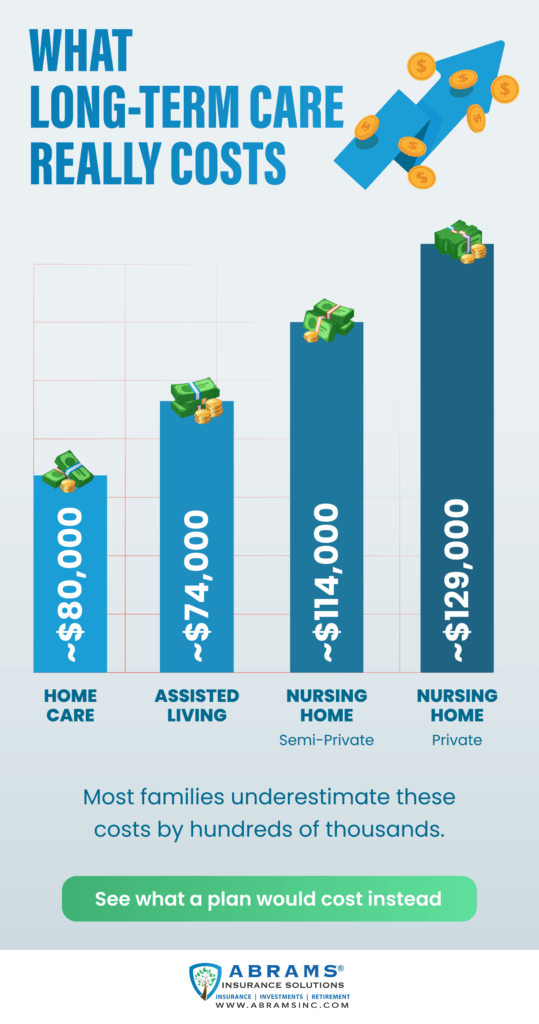

According to the latest 2025 Cost of Care Survey conducted by CareScout, a Genworth company, here’s what Americans are paying today for long-term care services:

| Type of Care | 2025 Annual Median Cost | Year-over-Year Change |

| Home Health Aide | $80,080 | Up 3% |

| Homemaker Services | $80,080 | Up 6% |

| Assisted Living Facility | $74,400 | Up 5% |

| Nursing Home (Semi-Private) | $114,975 | Up 2% |

| Nursing Home (Private) | $129,575 | Up 1% |

| Adult Day Health Care | $24,700 | Down 5% |

And costs are climbing. The Federal Long-Term Care Insurance Program’s 2024 Cost of Care Survey projects that, if care costs rise at even a modest 2.54% annual inflation rate, a nursing home that costs $112,420 today will cost nearly $186,000 annually in 20 years.

The average length of a long-term care need is approximately 2.5 to 3 years, but roughly 1 in 5 people who turn 65 will need care for 5 years or more. At today’s prices, a five-year nursing home stay at median costs totals over $630,000. Most families simply cannot absorb that kind of expense out of pocket.

Will Medicare or Health Insurance Pay for Long-Term Care?

This is one of the most common misconceptions in retirement planning. The short answer: probably not, and at least not in the way you’re hoping.

Medicare

Medicare is health insurance, not long-term care insurance. It will pay for up to 100 days of skilled nursing care following a qualifying hospital stay, but it does not cover custodial care (help with ADLs), and it does not pay for assisted living or home health aides in most situations. Once you’ve recovered from an acute illness, Medicare coverage ends.

Standard health insurance doesn’t cover it either. Health insurance covers medical treatment such as doctor visits, surgeries, and prescriptions, but it does not cover the ongoing personal assistance that defines long-term care.

Medicaid (Medi-Cal in California)

Medicaid does pay for nursing home care, but only after you’ve spent down most of your assets to qualify. In most states, that means drawing your savings down to $2,000 or less. In California (where Medicaid is called Medi-Cal), eligibility rules require you to be in a very low-income bracket before the government will step in. And even then, Medi-Cal dictates where you receive care, what type of care you receive, and how much of it you get.Long-term care insurance fills the gap that Medicare, Medicaid, and health insurance leave behind, and it does so while keeping you in control of your own care decisions.

Types of Long-Term Care Insurance

There are two main approaches to LTC coverage. Understanding the difference is key to making the right decision for your situation.

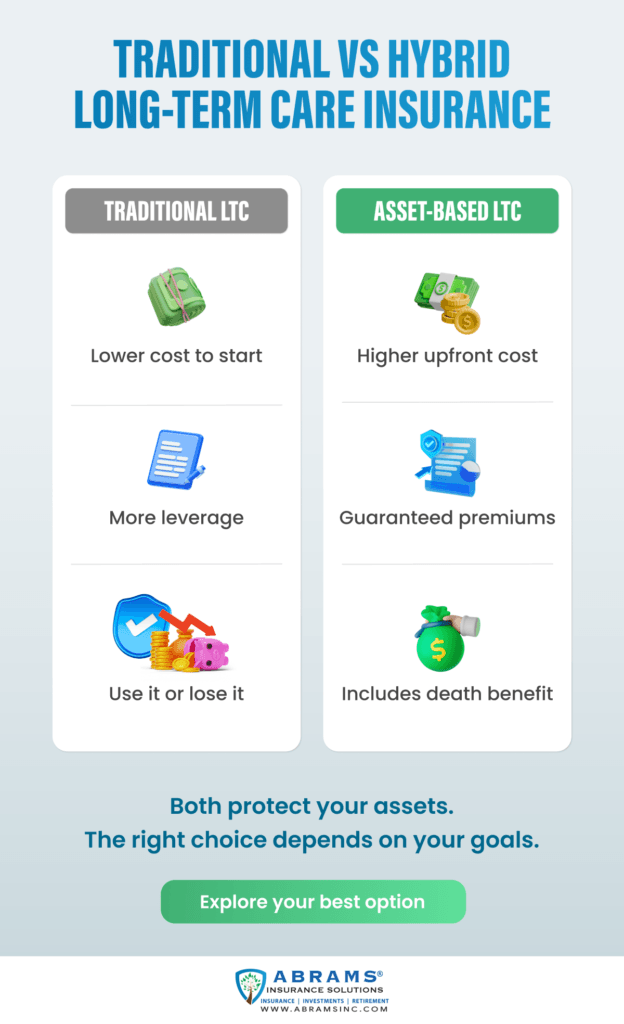

Traditional Long-Term Care Insurance

Traditional LTC insurance operates much like your home or auto coverage. You pay a regular premium to secure a specific pool of benefits; if you ever need care, the policy steps in to pay a daily or monthly amount up to your chosen limit.

This LTC type remains a popular choice for those who want to maximize their coverage for every dollar spent. Because these policies are highly customizable, you can tailor everything from the waiting period (elimination period) to inflation protection, ensuring the plan grows alongside your future needs.

One of the primary advantages of this route is the lower entry cost for significant coverage, which allows you to protect your assets without a large upfront investment. However, these policies follow a “use it or lose it” model; if you are fortunate enough never to need care, the premiums paid do not return to your estate.

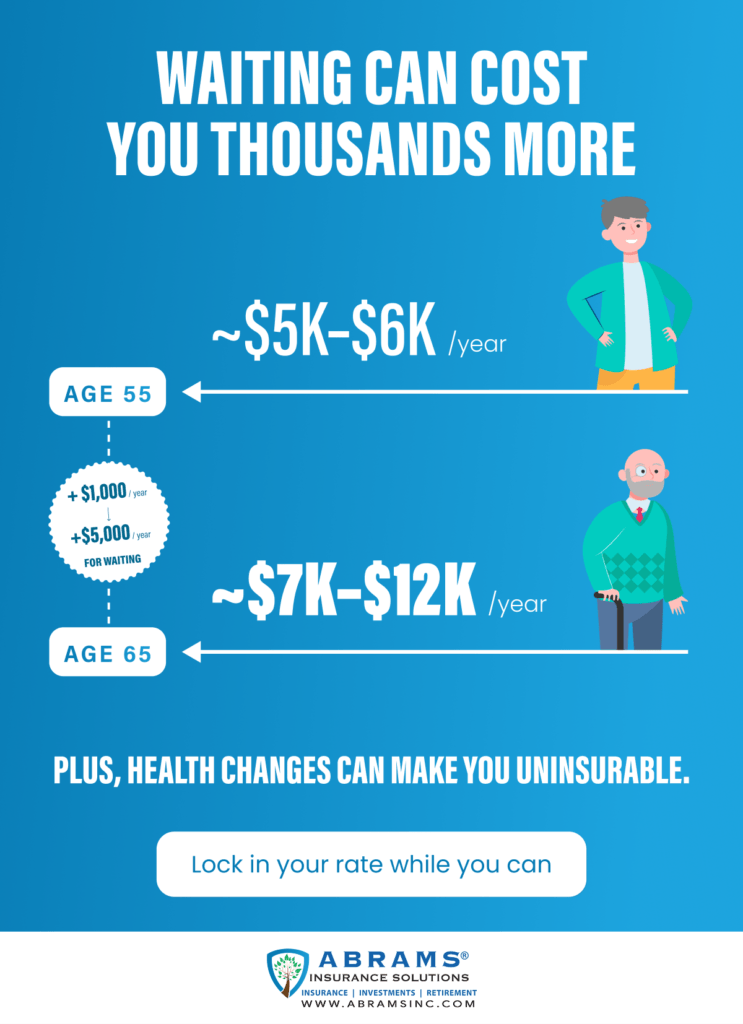

Timing plays a critical role in the cost of these plans. According to the American Association for Long-Term Care Insurance (AALTCI), a couple at age 55 might pay between $5,018 and $6,325 per year for a $165,000 benefit pool with 3% inflation protection. That same couple waiting until age 65 could see those annual premiums jump to between $7,137 and $12,250. Because rates vary significantly among providers, comparison shopping is essential to ensure you receive the best value for your protection.

Asset-Based (Hybrid) Long-Term Care Insurance

Hybrid policies, also called asset-based or linked-benefit policies, combine long-term care benefits with either life insurance or an annuity in a single package.

Here’s how they work: you fund the policy with either a single lump-sum premium or a series of premium payments. In return, you receive a pool of long-term care benefits that’s typically two to three times larger than what you paid in. If you never need long-term care, a life insurance death benefit passes to your beneficiaries. Either way, your money is not simply “lost.”

Hybrid policies have surged in popularity in recent years for one key reason: the use-it-or-lose-it objection disappears. Someone always benefits, whether it’s you, in the form of care benefits, or your loved ones, in the form of a death benefit.

Carriers offering strong hybrid LTC products include Nationwide, Lincoln Financial Group, Mutual of Omaha, and Pacific Life, among others.

Ready to explore hybrid coverage? Read our full guide: Asset-Based Long-Term Care: Protect Your Assets and Secure Your Future.

Short‑Term Care and Other Variations

For a more focused approach, short-term care policies offer a practical solution, typically providing up to one year of coverage. These plans often feature more affordable premiums and simplified medical qualifications, making them an accessible entry point for protection.

If you already own a permanent life insurance policy, you might have a built-in “backstop” through Accelerated Benefit or Chronic Illness Riders. These allow you to access a portion of your own death benefit early to help pay for care. While less comprehensive than a standalone policy, they provide a valuable layer of security.

Ultimately, many retirees find that a thoughtful combination of these flexible, smaller options, rather than a single “perfect” plan, is the most effective way to balance their budget with their need for peace of mind.

How Does LTC Insurance Work?

It’s important to remember that long-term care insurance is designed to step in when you truly need it, rather than at the first sign of a minor challenge. Understanding this process is key to ensuring your coverage is there for you exactly when it matters most.

Benefit Triggers

Insurance benefits are triggered when a licensed health professional certifies that you are unable to perform at least two activities of daily living without assistance or that you suffer from a severe cognitive impairment such as dementia. A nurse or social worker will typically perform an assessment and develop a plan of care. Once approved, benefits become payable after a waiting period.

Elimination Periods

Once a benefit trigger is met and certified by a physician, you enter the elimination period, which is the LTC equivalent of a deductible. This is a waiting period (typically 30, 60, or 90 days) during which you pay for care out of pocket before the insurance kicks in. Longer elimination periods mean lower premiums.

Some policies count calendar days, meaning the clock starts on the day you are certified, while others count service days only, days when paid care is actually received. Be sure to choose an elimination period that balances affordability with your ability to cover initial costs.

Daily or Monthly Benefit Amounts and Benefit Periods

After the elimination period, benefits begin paying out up to your daily or monthly benefit limit for as long as you need care, up to your policy’s maximum benefit period (often two, three, five years, or even unlimited lifetime). For example, if your policy pays $200 per day for up to 3 years, the total benefit pool is about $219,000. Once benefits are exhausted, you must cover additional costs yourself.

One powerful add-on worth discussing is the inflation protection rider. Given that care costs double roughly every 18–20 years, a policy purchased today without inflation protection may not stretch far enough by the time you actually need it. Compound inflation protection of 3% to 5% annually can dramatically increase the real-world value of your coverage over time.

How Much Does LTC Insurance Cost?

LTC premiums vary based on your age, health, gender, the benefit amount you choose, and the riders you add. Below are general benchmarks from the American Association for Long-Term Care Insurance (AALTCI):

| Age at purchase | Male annual premium | Female annual premium | Notes |

| Age 50 | ~$1,700/yr | ~$2,675/yr | Best value window |

| Age 55 | ~$2,050/yr | ~$3,200/yr | Still affordable |

| Age 60 | ~$2,800/yr | ~$4,400/yr | Higher but insurable |

| Age 65 | ~$3,750/yr | ~$5,900/yr | Limited options |

*Sample rates for a $165,000 benefit pool with 3% compound inflation protection. Actual rates vary by state, carrier, and health. Source: AALTCI 2023–2024.

** Women typically pay significantly more than men because they statistically live longer and file more claims. However, couples can save money by applying together through shared-care or spousal discount programs.

The Most Important Takeaway: Every year you wait costs you more. Waiting from age 55 to 65 permanently adds over $1,000 per year to a man’s premium and over $1,500 per year to a woman’s, for the life of the policy. More critically, a health event such as a new diagnosis of diabetes, heart disease, or early cognitive decline can disqualify you from coverage entirely. There is no appeals process once a carrier declines your application.

The best time to buy is when you’re young enough and healthy enough to qualify at a favorable rate.

How to Choose the Right Long‑Term Care Insurance Policy

Selecting the right policy requires balancing costs, benefits, and your personal circumstances. Here are key factors to consider:

- Age and health: Premiums are lowest if you apply in your mid‑50s and rise sharply as you age. Insurers may decline applicants with pre‑existing conditions. Waiting until your 60s or 70s can dramatically increase premiums or make you ineligible.

- Benefit amount and period: Estimate local care costs and decide on a daily or monthly benefit. A typical policy might provide $4 000–$6 000 per month for three or four years. Consider whether you want lifetime coverage, though premiums will be higher.

- Inflation protection: In your 50s or early 60s, it’s essential. Compound inflation riders (3% or 5%) keep benefits growing to keep pace with rising care costs. Simple inflation increases benefits by a fixed dollar amount each year but may not keep pace with real‑world cost increases.

- Elimination period: Choose a waiting period you can comfortably self‑fund. A 90‑day elimination period is common and saves money compared with a 30-day period.

- Shared care or joint policies: Couples may purchase policies that allow one spouse to use the other’s unused benefits if their own pool runs out. This option adds flexibility and may reduce overall premiums.

- Carrier financial strength and rate history: Insurers have raised rates on older policies because of low interest rates and higher claims. Choose a carrier with strong financial ratings and a reasonable history of rate increases. A specialist can help you evaluate the options.

Because premiums vary widely among insurers, it is important to request quotes from multiple carriers. As noted earlier, the difference between the lowest and highest premiums for identical coverage can exceed $5 000 per year.

Planning Ahead: When to Buy and What to Expect

Experts generally recommend purchasing long‑term care insurance in your mid‑50s to early 60s. At this age, premiums are still relatively affordable, and your health is more likely to meet underwriting requirements. As you age, you face a double whammy of higher premiums and a greater chance of being declined.

That said, every situation is different. Someone in excellent health at 68 may still qualify for good coverage at a reasonable rate. And certain hybrid products have more flexible underwriting than traditional policies.

The key is to get a personalized quote and assessment and not to assume you’ll deal with it later.

Underwriting Process

When you apply for coverage, insurers will evaluate your health through questionnaires, medical records, and possibly a phone or in‑person interview. They may review your prescription drug history and may require cognitive testing for applicants over a certain age. If you have pre‑existing conditions, you could be rated (charged a higher premium), offered limited benefits, or declined. Underwriting can take several weeks, so apply well before you anticipate needing care.

Tax Considerations

Premiums for tax‑qualified long‑term care policies are tax‑deductible up to certain limits based on your age. The Internal Revenue Service adjusts deduction limits annually. In some states, additional tax incentives or credits are available. Hybrid policies generally do not qualify for the same deductions because most of the premium is attributed to life insurance. Consult a tax professional to understand your specific situation.

Alternatives to Long‑Term Care Insurance

If you decide LTCI isn’t right for you, consider these alternatives:

Self‑funding: Some individuals choose to set aside assets or use retirement income to pay for future care. This option requires careful budgeting and may reduce the legacy you leave. You must also consider what happens if care costs exceed your estimates or if care lasts longer than expected.

Life insurance with LTC riders: Many permanent life insurance policies offer riders that allow you to accelerate the death benefit to pay for long‑term care. While this reduces the death benefit available to beneficiaries, it can provide flexibility. Premiums may be higher than traditional life insurance.

Annuities with LTC benefits: Certain annuities offer enhanced payouts if you need care. You invest a lump sum into the annuity, and it pays a higher monthly benefit if you meet LTC eligibility requirements. Unused funds may pass to heirs. However, returns may be lower than those of other investments.

Medicaid planning: For people with limited assets, working with an attorney to structure finances can help you qualify for Medicaid while protecting a portion of your wealth. This often involves complex rules and “look‑back” periods, so professional advice is necessary.

FAQs

Yes. LTC policies usually pay benefits if a licensed professional certifies that you cannot perform two activities of daily living or you have a severe cognitive impairment. Alzheimer’s disease, Parkinson’s disease, and other dementias meet this requirement.

With a traditional LTC policy, premiums are typically not refunded if you never use the coverage. Some insurers offer return‑of‑premium riders or nonforfeiture benefits that guarantee you receive some value if you cancel the policy. Hybrid life/LTC policies always pay either a long‑term care benefit or a death benefit.

Many carriers offer shared care riders that allow couples to pool their benefits. If one spouse exhausts their individual pool, they can tap into the other spouse’s remaining benefits. This adds flexibility but increases premiums.

Premiums for tax‑qualified policies are tax‑deductible as a medical expense, subject to age‑based limits. For example, taxpayers aged 60–69 could deduct up to $4830 (2024 IRS limit) as a medical expense. Hybrid policies generally do not receive the same tax treatment.

Traditional LTC insurance policies may include a nonforfeiture option, which provides a limited paid‑up policy or return of a portion of premiums. Hybrid policies usually have a cash value that grows over time; if you cancel, you can surrender the policy and receive the accumulated value.

Taking the Next Step: Protecting Your Future

Long-term care is one of the most significant financial risks most families face in retirement. The good news is that there are smart, flexible tools available to manage that risk, whether through traditional coverage, a hybrid policy, or a custom strategy that fits your broader retirement plan.

At Abrams Insurance Solutions, we pride ourselves on acting as an independent long-term care insurance agent. Our team is licensed in all 50 states and represents over 70 top-rated insurance companies. Because we aren’t tied to a single provider, we do the comparison shopping for you to find the best value and fit, completely obligation-free.

When you’re ready to see how these strategies look for your specific situation, a long-term care insurance specialist can help you navigate the nuances of each policy. Simply use the form on this page to request your personalized long-term care insurance quote, or call us at 858-703-6178 to speak directly with a long-term care insurance specialist today.