Best Ways to Find Affordable Health Insurance

Posted in Health Insurance last updated on February 18, 2026

Posted in Health Insurance last updated on February 18, 2026Affordable health insurance takes some legwork. But it’s within reach and even fairly fast if you get your priorities straight and ask for help.

We will cover all the basics, terminology, and strategies for finding the right health coverage at the lowest possible price.

If you want to get help from a knowledgeable insurance advisor, please click here to request help. We will then get in touch with you to review the best health insurance options for your situation.

Table of contents

- Quick Summary

- How Health Insurance Works

- What Does Health Insurance Cover?

- Plan Meanings Under the Affordable Care Act

- Plan & Network Types

- What is Open Enrollment?

- Medi-Share Alternative Health Insurance Options

- How to Choose the Best Affordable Health Insurance Policy

- 4 Easy Ways to Save Money on your Health Insurance

- Conclusion

- Where to Get Help

Quick Summary

Health insurance plans can vary greatly, and the coverage you need will depend on your health and specific wants and needs. Knowing the different types of coverage, what the insurance pays, and the deductible amount is the most important step to saving money on your health insurance and preventing high medical costs. You may even qualify for health insurance coverage outside of open enrollment.

How Health Insurance Works

At its core, health insurance spreads the cost of getting sick or injured among a group of people. If you have 100 people, records show that a certain percentage will be ill or injured at any given time. The larger the group of people, the more predictable the numbers become.

So if an insurance company knows that 5 out of the 100 will be sick this year, they also know roughly how much they’ll need to pay to cover that. So you and I, two of the 100 people, only need to pay 2% of whatever the sickness will cost, and if something happens, we get covered out of that pool of money.

Easy, in theory.

Of course, more factors are now involved, but that’s the basics.

What is a premium?

What you and I will experience is paying the insurance company each month, called the premiums. Most plans work with monthly premiums, but many offer other payment timetables too.

When we go to the hospital, we will likely have a copay. That means an upfront cost for the visit we share with the insurance company.

What is a deductible?

Then there’s a deductible on many plans. That’s how much we pay out of pocket before the insurance company covers the rest. There’s an annual reset timer.

For example, if your deductible is $3,000 for the year, you will pay the first $3,000 in medical expenses, then your health insurance company will take over payments after that.

There are advantages to deductibles, although they vary depending on your current health and financial situation.

Plans with higher deductibles virtually always have lower premiums. Need to pay less each month? Relatively healthy? A high-deductible plan might make the most sense.

High-deductible plans also lead to some tax advantages.

Pairing a high deductible plan with a Health Savings Account (HSA) can lead to some great tax breaks next year.

But here’s the best part. The money in the HSA stays in the account and can be invested and grown each year. Then, after you’ve built up some growth in the account, it can go toward medical expenses without any tax on the growth. Awesome.

By the way, a Flexible Spending Account (FSA) does not work the same way. If you don’t spend all of the money in your FSA by the end of the year, you lose it.

What Does Health Insurance Cover?

Thanks to the Affordable Care Act (AKA Obamacare), health insurance companies are now required to cover what’s called the 10 Essentials. Before, health insurance companies could cover (or not cover) whatever they wanted, making picking an affordable health insurance plan an enormous pain.

These 10 essential health benefits cover the following:

- Ambulatory patient services

- Emergency services

- Hospitalization

- Pregnancy, maternity, and newborn care (including birth control and breastfeeding care)

- Mental health and substance use disorder treatment (including behavioral health)

- Prescription drugs

- Rehabilitative and habilitative services/devices

- Laboratory services

- Preventative and wellness services & chronic disease management

- Pediatric services, including oral and vision

Dental coverage is not required but can usually be added to a plan.

Even if your major medical plan checks the big boxes, many families add vision coverage to reduce costs for exams, glasses, and contacts.

VSP Vision Insurance: Coverage Options, Plan Choices, and Costs Explained

Vision insurance is often overlooked when evaluating overall health coverage options, yet routine eye exams and preventive doctor visits can detect serious health issues early and help reduce unexpected medical bills. VSP is one of the most recognized vision insurance providers in the country, offering multiple plan choices for individuals and families of all sizes.

Before selecting coverage, it is important to review network access, frame allowances, premium costs, and how different coverage options align with your family size and budget. Understanding the enrollment process and comparing affordable health insurance options for vision care can make preventive services, glasses, and contacts far more manageable financially.

Is VSP vision insurance good? Learn about plans, benefits, and savings to decide if it’s the right vision coverage for you.

How Delta Dental Insurance Works (Qualified Plans, Dental Plans, and Coverage Options)

Dental plans can significantly reduce medical bills related to cleanings, fillings, crowns, root canals, and major procedures. Delta Dental is one of the largest dental insurance providers, offering multiple coverage options and plan choices depending on your state, family size, and budget.

If you are evaluating Delta Dental as part of a broader qualified health plan strategy or exploring standalone dental plans, understanding PPO vs. HMO structures, waiting periods, annual maximums, and the enrollment process is essential. Selecting the right low-cost coverage can protect your family from unexpected dental expenses while keeping premiums manageable and making routine dental visits more affordable.

Simple guide to how Delta Dental works, what each plan covers, expected costs, and how to save the most by choosing in-network dentists.

Plan Meanings Under the Affordable Care Act

When you first go to the insurance marketplace, you’ll see different types of plans named after metals.

First, this is not the quality of care or the plan. It’s the cost.

- Bronze Plan – 60/40 split, lowest premiums, best for healthy people or unlikely to use insurance

- Silver Plan – 70/30 split, moderate premiums, best for routine care

- Gold Plan – 80/20 split, higher premiums, best for lots of care and low out-of-pocket costs

- Platinum Plan – 90/10 split, highest premiums, best for frequent medical care

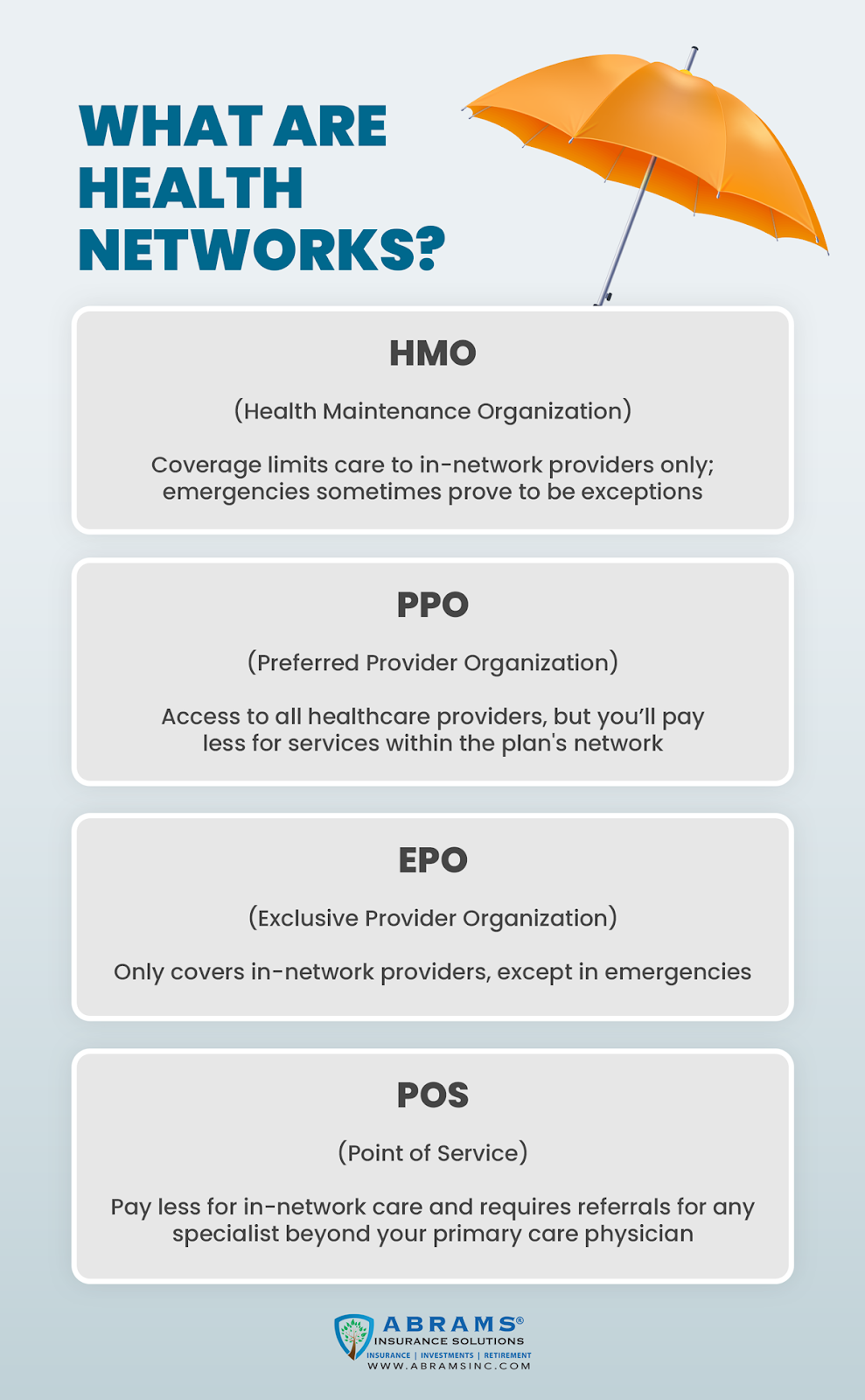

Plan & Network Types

Another consideration point is the types of plans and what healthcare providers they allow you to access. You’re probably seeing things like PPO or HMO, but there are other less common ones as well.

These boil down to where your health insurance will cover medical treatment. You’ll see references to in-network and out-of-network here.

- HMO (Health Maintenance Organization) – Coverage limits care to in-network providers only; emergencies sometimes prove to be exceptions

- PPO (Preferred Provider Organization) – Access to all healthcare providers, but you’ll pay less for services within the plan’s network

- EPO (Exclusive Provider Organization) – Only covers in-network providers, except in emergencies

- POS (Point of Service) – Pay less for in-network care and requires referrals for any specialist beyond your primary care physician

What is In-Network vs. Out-of-Network?

Clinics, hospitals, and other care centers will belong to different insurance networks. It all depends on how they want to set up their billing. Typically, the more affordable health insurance heavily emphasizes going to in-network providers.

In-network means they’ll take your insurance at the rate they agreed upon with the insurance company. Out-of-network means they get to charge you full price unless your health insurance has some level of out-of-network health care coverage.

What is Open Enrollment?

Open enrollment happens at the end of the calendar year, usually November through about mid-December, depending on the year.

It lets you switch plans or get a new one without having one of the qualifying life events that trigger a special enrollment period.

You can get a different healthcare plan or change health insurance if you have a qualifying event outside the open enrollment period. For example, if you:

- Lose your current healthcare cover

- Get married/divorced

- Have or adopt a child

- Move to a different zip code/county

However, not everyone wants a traditional marketplace plan. Here’s an alternative some families consider during open enrollment.

Medi-Share Alternative Health Insurance Options

Looking for affordable health insurance options after a major life change such as marriage, a new baby, job loss, or relocation? Health sharing programs like Medi-Share have become increasingly popular for individuals and families seeking lower monthly costs and low-cost coverage options outside of a qualified health plan. However, these programs are not ACA-qualified health plans and come with important limitations, especially when it comes to doctor visits and how medical bills are shared.

If you are comparing health sharing ministries versus traditional coverage options, it is critical to understand eligibility guidelines, the enrollment process, reimbursement structures, family size considerations, and how routine doctor visits or larger medical bills are handled before enrolling. Choosing between different plan choices can significantly impact your out-of-pocket exposure and long-term protection.

Explore Medi-Share, a faith-based healthcare solution and trusted alternative to health insurance during Open Enrollment.

How to Choose the Best Affordable Health Insurance Policy

First, identify how much care you think you’ll need in a year.

A lower-premium, high-deductible plan would probably be a good fit if you’re relatively healthy and only need coverage to protect against the cost of a surprise medical event.

On the other hand, if you have a pre-existing condition that requires regular medical care, you’ll probably save more money in the long run by choosing a plan with higher premiums that protects you from more out-of-pocket expenses.

Next, move on to any healthcare providers you currently work with. Whether they’re in or out of network will help you decide which plan has the right network for you.

That will also help you determine which type of plan is a good fit.

Finally, it comes down to balancing the premiums versus the features you want. It’s always a good idea to ask for help.

You can also get outside coverage for severe health conditions through critical illness insurance, which provides a lump sum for things like a cancer diagnosis or chronic illnesses.

4 Easy Ways to Save Money on your Health Insurance

If you’re like most people, then you may often worry about the rising healthcare costs. Here are a few quick and easy tips that can save you hundreds, if not thousands, of dollars on your health insurance premiums.

Find out if you qualify for a subsidy. The Patient Protection and Affordable Care Act (Affordable Care Act) is a federal law that provides affordable health insurance to more Americans. It is also known as Obamacare or ACA. This law provides increased benefits and requires that all Americans have health insurance or face a penalty. It also provides financial help and tax credits for qualified health plans.

Increase your deductible. This is one of the quickest ways to lower your premiums. The difference between a $500 deductible and a $5,000 deductible would amount to significant monthly savings.

Work with an agent or broker. Agents can get you quotes from multiple insurance companies and can help you compare the benefits and costs of each plan. Best of all, working with a health insurance agent will cost you nothing, and having an expert on your side can save you money.

Consider a High Deductible Health Plan (HDHP) and Health Savings Account (HSA). HDHPs typically have lower premiums and higher deductibles than traditional health plans. Once the deductible is met, there is typically no additional out-of-pocket expense during that calendar year, and the deductible is waived altogether for preventive care.

Opening an HSA (a tax-advantaged medical savings account) requires enrollment in a qualified HDHP. The funds contributed to an HSA are not subject to federal income tax at the time of deposit or upon withdrawal when used for qualified medical expenses. The funds earn interest and roll over and accumulate year to year if not spent.

Conclusion

Health insurance can be quite the learning curve. But it is doable on your own if you don’t have health insurance through your employer. Low-cost insurance options and marketplace subsidies can help families reduce their monthly premium, depending on income level.

Affordable health insurance coverage starts with determining what type of health care plan you and any family members will use. Lower costs typically come with high-deductible plans, which work well as insurance against the cost of health emergencies. The cost of coverage increases the more thorough coverage you’re looking for or if you want more preventive care services.

Where to Get Help

Heathcare.gov has excellent service options for getting extra assistance. However, we don’t recommend waiting until the last couple of days of open enrollment when everyone else is trying to call in too.

You can get more specialized help finding affordable health insurance by working with an insurance agent. The state sets the limit on what a health insurance policy can cost so that it won’t cost you anything more.

For help getting great, affordable health insurance, click here and we will be in touch to help guide you to the best plan for your situation.